The U.S. residence insurance coverage trade has skilled an upward development in all-peril loss prices over the previous seven years, in accordance with a brand new report launched by LexisNexis Threat Options.

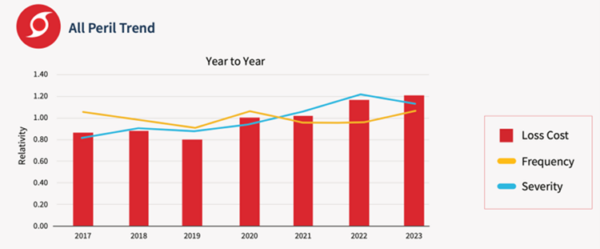

The ninth annual LexisNexis U.S. Residence Traits Report discovered that all-perils misplaced prices and all-perils frequency elevated by 4.1 p.c and 11 p.c, respectively, from 2022 to 2023. Since 2019, all-perils loss prices rose 52 p.c, with frequency climbing 16.9 p.c.

Though severity has declined 6.3 p.c since 2022, it stays 29.8 p.c larger than 2019 figures, the information confirmed.

For the needs of the report, the all-perils figures mix information for hail, wind, water, fireplace and lightning climate perils, in addition to non-weather associated claims corresponding to water leaks, thefts or legal responsibility.

Disaster claims represented 46 p.c of claims throughout all perils mixed in 2023, the very best in seven years.

By peril, among the information breaks down as follows:

- Hail loss prices elevated 57.9 p.c from 2022 to 2023, together with frequency (up 53.6 p.c) and severity rising 2.8 p.c 12 months over 12 months from 2022. States with the very best influence of hail-related perils embrace Colorado, Nebraska and Wyoming.

- Loss prices for different weather-related perils declined from 2022 to 2023, with fireplace and lightning prices down 11.1 p.c, and weather-related water down 51.4 p.c.

- Non-weather-related water loss prices decreased by 11.2 p.c in the identical interval however remained on an upward development over the previous seven years.

“Within the final 12 months, the U.S. noticed a number of historic-level climate catastrophe occasions and the very best stage of catastrophic claims throughout all perils we’ve seen previously seven years, which contributes to rising premiums that customers throughout the nation face proper now,” stated Cole Winans, vice chairman, residence insurance coverage, LexisNexis Threat Options.

“As residence insurance coverage carriers proceed to take care of seasonal and geographic variabilities associated to local weather— along with rising inflation, materials and labor value—understanding by-peril and macro stage residence insurance coverage tendencies, coupled with sustaining intensive information and imagery on present home situations over an prolonged time period is crucial to stay nimble in at present’s risky and dynamic market,” he added.

“At the same time as extra insurers are more likely to see fee will increase accepted in sure states within the coming months, they’ll have to be discerning in writing new enterprise solely in these pockets the place they’ll achieve this profitably and that will probably be on a carrier-by-carrier and state-by-state foundation.”

Regardless of the all-perils severity discount in 2023 (6.3 p.c down from 2022), the elevation in severity above 2019 (up 29.8 p.c) factors to the significance of long-term development information when evaluating threat and pricing, the report said.

Colorado ranks highest in loss prices from catastrophic claims (274 p.c above 2023 U.S. common catastrophic loss value), whereas the severity of claims ({dollars} misplaced, on common, per declare paid) was highest within the state of Hawaii in 2023 (63 p.c above 2023 U.S. common severity).

U.S. states with the very best mixed disaster and non-catastrophe loss prices embrace Colorado, Minnesota, Nebraska, Louisiana and Iowa. Lowest rating states embrace Massachusetts., New Hampshire, West Virginia, Vermont and Maine.

In 2023, the information indicated the U.S. skilled 6,962 hail occasions, up 57.3 p.c from 2022, with 71 p.c of hail claims deemed catastrophic.

With 28 climate and local weather disasters in 2023, every surpassing the billion-dollar harm threshold, 17 have been attributed to extreme climate or hail occasions.

Hail peril seasonality over the previous seven years continues, with April, Could and June observing the very best frequency and loss value in 2023.

Wind peril frequency rose 14.8 p.c, together with a loss value growing 0.7 p.c from 2022-2023. Severity, by comparability, fell 12.3 p.c year-over-year, the report discovered. Regardless of seasonal loss value averages peaking in August and September over the previous seven years, 2023 loss value and frequency have been highest in March.

In 2023, 62 p.c of wind claims have been deemed catastrophic claims, up from 52 p.c the 12 months prior.

Fireplace and lightning perils in 2023 noticed decreases in loss prices (-11.1 p.c), frequency (-8.6 p.c) and severity (-2.7 p.c) from 2022. Nevertheless, catastrophic claims rose 7 p.c from 2023, with the Maui, Hawaii, wildfire thought-about probably the most damaging and lethal occasions in 2023.

Climate-related water perils declined in 2023 with a discount in loss value (-51.4 p.c), frequency (-25.5 p.c) and severity (-34.8 p.c). In 2023, 61 p.c of weather-related water claims have been catastrophic.

Addressing claims associated to water harm, corresponding to leaking pipes and home equipment, non-weather-related Water perils decreased throughout loss value (-11.2 p.c), frequency (-10.3 p.c) and severity (-1.1 p.c) in 2023.

Whereas theft loss value and frequency decreased by 14.2 p.c and 15.8 p.c, respectively, in 2023, severity rose by 1.9 p.c, partially attributed to the rising value of shopper items corresponding to high-end kitchenware.

Legal responsibility noticed a marginal improve in severity (0.2 p.c) in 2023, with an 18.3 p.c drop in frequency driving down general loss prices (down 18.2 p.c).

Different perils, together with bodily harm claims not included elsewhere, prolonged protection, harm to property of others, and many others., noticed a frequency improve of 9.3 p.c year-over-year. Loss prices, together with severity, each declined 10.7 p.c and 18.3 p.c, respectively, from 2022 to 2023.

“Once we take a look at peril information over a seven-year span, it’s more and more clear that residence insurers can’t depend on short-term tendencies alone to make absolutely knowledgeable selections about their books of enterprise and operational methods,” stated George Hosfield, affiliate vice chairman, residence insurance coverage, LexisNexis Threat Options. “For instance, whereas hail loss value surged by 57.9 p.c in a one-year observance, the longer-term development exhibits constant will increase throughout all perils year-over-year. This emphasizes the necessity for carriers to think about broader historic information when evaluating threat and adjusting pricing methods to assist assist their long-term profitability.”

Subjects

Traits

Pricing Traits

Householders

{kind=link}